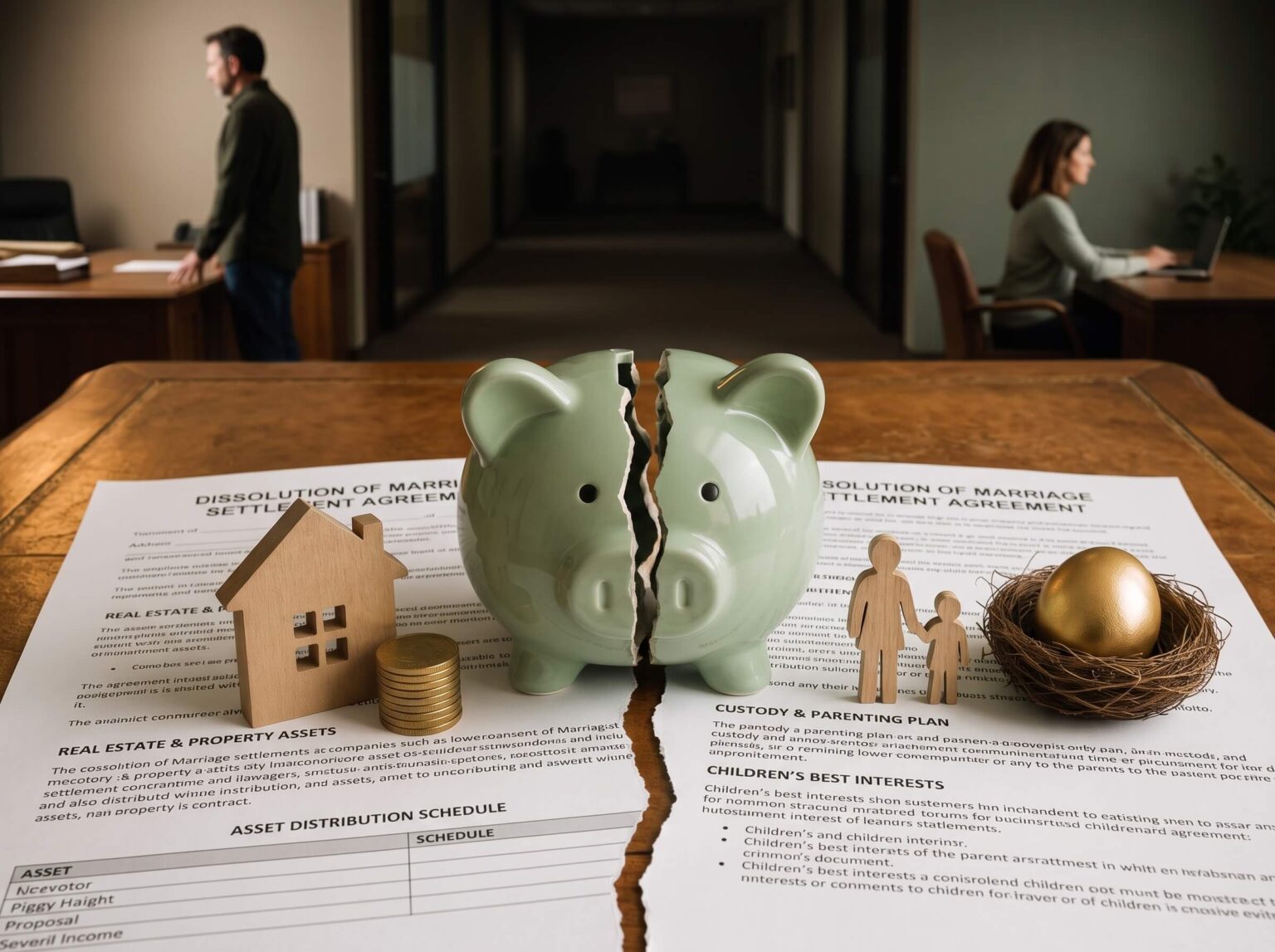

Ask someone going through a divorce what they are worried about, and you’ll usually hear the same answers.

- The house.

- The children.

- The savings.

- The mortgage.

Very few people immediately mention their pension. Ironically, that pension could be worth far more than everything else they own.

One of the biggest financial mistakes made during divorce in the United Kingdom is treating pensions as an afterthought. Many separating couples spend months arguing over who keeps the family home while barely discussing the retirement savings that may ultimately be worth several times more than the property’s equity.

Due to the fact pensions are invisible—they cannot be lived in, driven, or displayed—they are often ignored until it is too late. This guide exists to change that. Whether you live in England, Scotland, Wales or Northern Ireland, understanding how pensions are treated during divorce could affect your financial security for decades after your marriage ends.

A divorce may last months. The consequences of a poor pension settlement can last the rest of your life.

Divorce Ends a Marriage—Not Your Financial Responsibilities

Many people assume that once a divorce is final, every financial connection between two spouses automatically disappears.

That is not how UK law works.

A divorce legally ends the marriage, but it does not automatically end financial claims between former spouses or civil partners. Financial matters—including pensions, property, investments, savings, debts and maintenance—must either be agreed between the parties or determined by a court.

In England and Wales, for example, obtaining a Final Order (formerly called a Decree Absolute) does not, by itself, prevent future financial claims. A separate financial settlement, usually approved by the court, is needed to achieve a legally binding resolution.

Scotland and Northern Ireland have different procedures and legal rules, but pensions are still recognised as financial assets that may need to be addressed when a relationship legally ends. This distinction surprises many people.

A person may think:

“We’ve divorced, so surely what’s mine is mine.”

Legally, that assumption can be wrong. One of the central themes throughout this guide is that divorce has two separate dimensions:

- the legal ending of the marriage; and

- the financial ending of the relationship.

These often happen at different times. Understanding that distinction is the first step towards understanding pensions.

Why Pensions Matter So Much

Imagine two couples.

Couple A

They own:

- a house worth £400,000

- £20,000 in savings

- two cars

- furniture

- no pensions

Their wealth is easy to see.

Now imagine

Couple B

- They rent their home.

- They own one modest car.

- They have £5,000 in savings.

On paper they look much poorer. But one spouse has spent thirty-five years working for the NHS and has built up a valuable defined benefit pension.

The other has a workplace pension worth £180,000. Together, their pensions could be worth well over one million pounds, depending on the benefits they provide. From the outside, they appear less wealthy than Couple A.

In reality, they may be considerably wealthier. This is why family courts do not look only at visible assets. They examine all assets. That includes pensions.

MoneyHelper—the government-backed financial guidance service—warns that pensions are frequently one of the largest assets in a marriage and may even be worth more than the family home, yet many people fail to include them properly when negotiating a financial settlement.

The Hidden Nature of Pension Wealth

Unlike a bank account, you cannot usually log into your pension and immediately spend the money. Unlike a house, you cannot walk around it. Unlike a car, you cannot drive it. A pension is, in many ways, invisible wealth.

It represents money that has been saved and invested for your future retirement. Some pensions hold an actual investment fund. Others promise to pay a guaranteed income for life.

Either way, they have value. Sometimes enormous value. Think of a pension like planting an oak tree. You cannot enjoy its shade immediately. For years it simply grows quietly beneath the surface. Then, decades later, it becomes one of the biggest things you own.

Divorce often forces people to look at that tree for the first time.

Why Courts Treat Pensions as Assets

Suppose one spouse worked full-time for thirty years while the other stayed home raising children. The working spouse paid into a pension every month. The stay-at-home parent did not.

At first glance, it might appear that only one person “earned” the pension. UK family law generally takes a broader view. Marriage is recognised as an economic partnership. One person’s career may only have been possible because the other cared for children, managed the household, supported relocations, or sacrificed their own career opportunities.

Because of this, pensions accumulated during the relationship are often treated as assets to be considered when dividing the couple’s finances. They are not automatically split, nor automatically ignored; instead, they form part of the overall financial picture that the parties or the court must examine.

This principle is important because it explains why someone who never paid directly into a pension may still have a legitimate claim relating to it. That does not mean they automatically receive half. It means the pension forms part of the overall financial settlement.

How much, if any, is ultimately shared depends on many factors that vary by jurisdiction and by the facts of the case.

A Pension Is Not Just “Old Age Money”

Children often understand money as something you can spend today. Adults often think about money in two different ways:

- money for today; and

- money for tomorrow.

A pension is tomorrow’s money. It exists to provide financial security after you stop working. That is why pensions deserve special attention during divorce.

Imagine a couple who agree that one spouse will keep the family home while the other keeps a pension worth roughly the same amount. On paper, the values may appear equal. In reality, they are very different assets.

A house provides somewhere to live today. A pension provides income many years into the future. Comparing them is a little like comparing apples and bicycles. Both have value. Both are useful. But they serve completely different purposes.

One of the recurring themes throughout this guide is that assets with the same monetary value are not necessarily equal in practical value.

Why So Many People Ignore Their Pension During Divorce

Financial advisers often describe pensions as the “forgotten asset” in divorce. There are several reasons for this. First, pensions are complicated. Many people do not fully understand their own pension, let alone their spouse’s.

Second, retirement can seem very far away. Someone aged forty-five may naturally focus on where they will live next month rather than what will happen at age sixty-seven.

Third, people often underestimate the value of pensions because they think only about monthly contributions rather than decades of investment growth or promised future income.

Finally, divorce is emotionally exhausting. People frequently prioritise immediate stability over long-term financial security. It is perfectly understandable why someone fighting over custody arrangements, housing or day-to-day living costs may not immediately think about retirement income twenty years from now.

Unfortunately, overlooking pensions during divorce can create financial problems that only become apparent decades later.

The Biggest Myths About Pensions and Divorce

One reason pensions are frequently misunderstood is that myths spread much faster than facts. Throughout this guide, we will separate common misconceptions from the legal reality.

Myth 1: “My pension belongs only to me because I earned it.”

This is probably the most common misconception. Although the pension is legally in one person’s name, the value of that pension can still be considered during divorce proceedings as part of the financial settlement.

The court does not simply ask who paid into it; it considers the wider circumstances and the applicable legal rules.

Myth 2: “My spouse automatically gets half my pension.”

No. There is no automatic rule in UK law stating that pensions must always be divided equally. The court’s objective is fairness under the relevant legal framework, and fairness does not necessarily mean a 50:50 division.

In some cases there may be no pension sharing at all; in others, a different percentage may be appropriate depending on the couple’s overall financial circumstances.

Myth 3: “Only private pensions count.”

Incorrect. State Pension rights may also be relevant in some divorce cases, although they are dealt with under separate legal rules from private and workplace pensions. Depending on the circumstances, the court may require information about State Pension entitlement when considering the overall financial settlement.

Myth 4: “If we don’t mention the pension, it stays untouched.”

Ignoring a pension does not necessarily protect it. Instead, failing to identify and properly value pension rights can lead to an unfair financial settlement that may significantly affect retirement security. MoneyHelper strongly recommends including pensions when considering the division of assets on divorce or dissolution.

Myth 5: “The family home is always the most valuable asset.”

Sometimes it is. Often it is not. For many long-serving teachers, NHS employees, police officers, firefighters, civil servants, military personnel and private-sector professionals, pension rights may represent the largest single asset accumulated during the marriage.

Thinking About Marriage as a Financial Partnership

One of the easiest ways to understand divorce law is to stop thinking about marriage solely as a romantic relationship. Legally, marriage also creates an economic partnership. Imagine two friends opening a business together.

One manages sales. The other handles accounts. At the end of ten years, the business succeeds because both contributed in different ways. Marriage often works similarly.

- One spouse may earn more.

- The other may care for children.

- One may relocate to support the other’s career.

- Another may reduce working hours to care for elderly relatives.

These contributions are different. They are not necessarily unequal. That idea—that marriage is a partnership rather than simply two separate financial lives—helps explain why pensions are considered alongside homes, savings and investments during divorce.

It also explains why understanding pensions is not merely a matter for accountants or lawyers. It is a matter of long-term financial security.

The Most Important Lesson to Remember

If you remember only one thing from this chapter, let it be this:

A pension is not simply money for retirement. During divorce, it is a financial asset that may influence the entire settlement.

It may determine:

- where you live after divorce;

- when you can afford to retire;

- how comfortably you live in later life;

- whether you remain financially independent in old age; and

- the standard of living you enjoy decades after the divorce itself has become a distant memory.

That is why pensions deserve careful attention from the very beginning of any divorce process—not as an afterthought, but as one of the central pieces of the financial puzzle.

The chapters that follow will build on this foundation. Before examining how pensions are divided, shared, offset or valued by the courts, we must first understand what a pension actually is, because not all pensions work in the same way—and the differences can dramatically affect the outcome of a divorce.